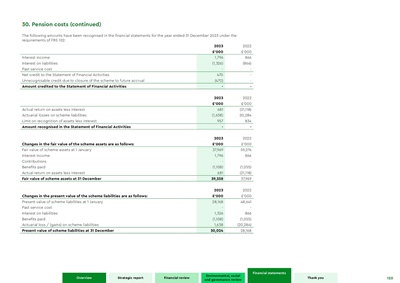

30. Pension costs (continued)

The following amounts have been recognised in the financial statements for the year ended 31 December 2023 under the

requirements of FRS 102:

2023 2022

£'000 £'000

Interest income 1,796 866

Interest on liabilities (1,326) (866)

Past service cost - -

Net credit to the Statement of Financial Activities 470 Unrecognisable

credit due to closure of the scheme to future accrual (470) -

Amount credited to the Statement of Financial Activities - -

2023 2022

£'000 £'000

Actual return on assets less interest 681 (21,118)

Actuarial losses on scheme liabilities (1,638) 20,284

Limit on recognition of assets less interest 957 834

Amount recognised in the Statement of Financial Activities - -

2023 2022

Changes in the fair value of the scheme assets are as follows: £'000 £'000

Fair value of scheme assets at 1 January 37,969 59,276

Interest income 1,796 866

Contributions - Benefits

paid (1,108) (1,055)

Actual return on assets less interest 681 (21,118)

Fair value of scheme assets at 31 December 39,338 37,969

2023 2022

Changes in the present value of the scheme liabilities are as follows: £'000 £'000

Present value of scheme liabilities at 1 January 28,168 48,641

Past service cost - Interest

on liabilities 1,326 866

Benefits paid (1,108) (1,055)

Actuarial loss / (gains) on scheme liabilities 1,638 (20,284)

Present value of scheme liabilities at 31 December 30,024 28,168

120

Environmental, social

and governance review

Financial review

Strategic report

Overview

Financial statements

Thank you